What Are Payment Systems? PSP, Payment Gateway and Orchestration Explained

Payment gateway, PSP or payment orchestration — what does your business actually need? A complete guide to payment infrastructure concepts and Turkey's payment ecosystem.

As digital commerce grows, payment infrastructure has become a strategic asset rather than a commodity. Whether you run an e-commerce site, a SaaS product or a platform business, understanding the difference between a payment gateway, a PSP and payment orchestration helps you make the right infrastructure decision.

What Is a Payment System?

A payment system is the complete infrastructure that enables the secure, fast transfer of funds between buyer and seller. Every card transaction involves four key players:

- Cardholder: The person making the payment.

- Merchant: The business receiving the payment.

- Acquirer Bank: The merchant's bank — provides the virtual POS infrastructure.

- Issuer Bank: The cardholder's bank — approves or declines the transaction.

Card networks (Visa, Mastercard) manage the messaging between acquirer and issuer.

What Is a Payment Gateway?

A payment gateway is the technology layer that encrypts card data and routes it to the acquirer bank. It's the digital equivalent of a physical POS terminal. Its core functions:

- Encrypt and transmit card data (SSL/TLS)

- Manage 3D Secure authentication

- Return approval or decline to the merchant

- Support transaction types: sale, cancel, refund, pre-authorisation

What Is a PSP (Payment Service Provider)?

A PSP enables merchants to connect to multiple banks or card networks through a single integration, handling both the gateway and acquiring bank relationships. Examples in Turkey: iyzico, PayTR, Paratika.

Advantages: Fast integration, low startup cost, technical infrastructure managed by PSP.

Limitations: Merchant cannot control which bank processes each transaction. No dynamic routing across multiple banks. Flexibility decreases as transaction volume grows.

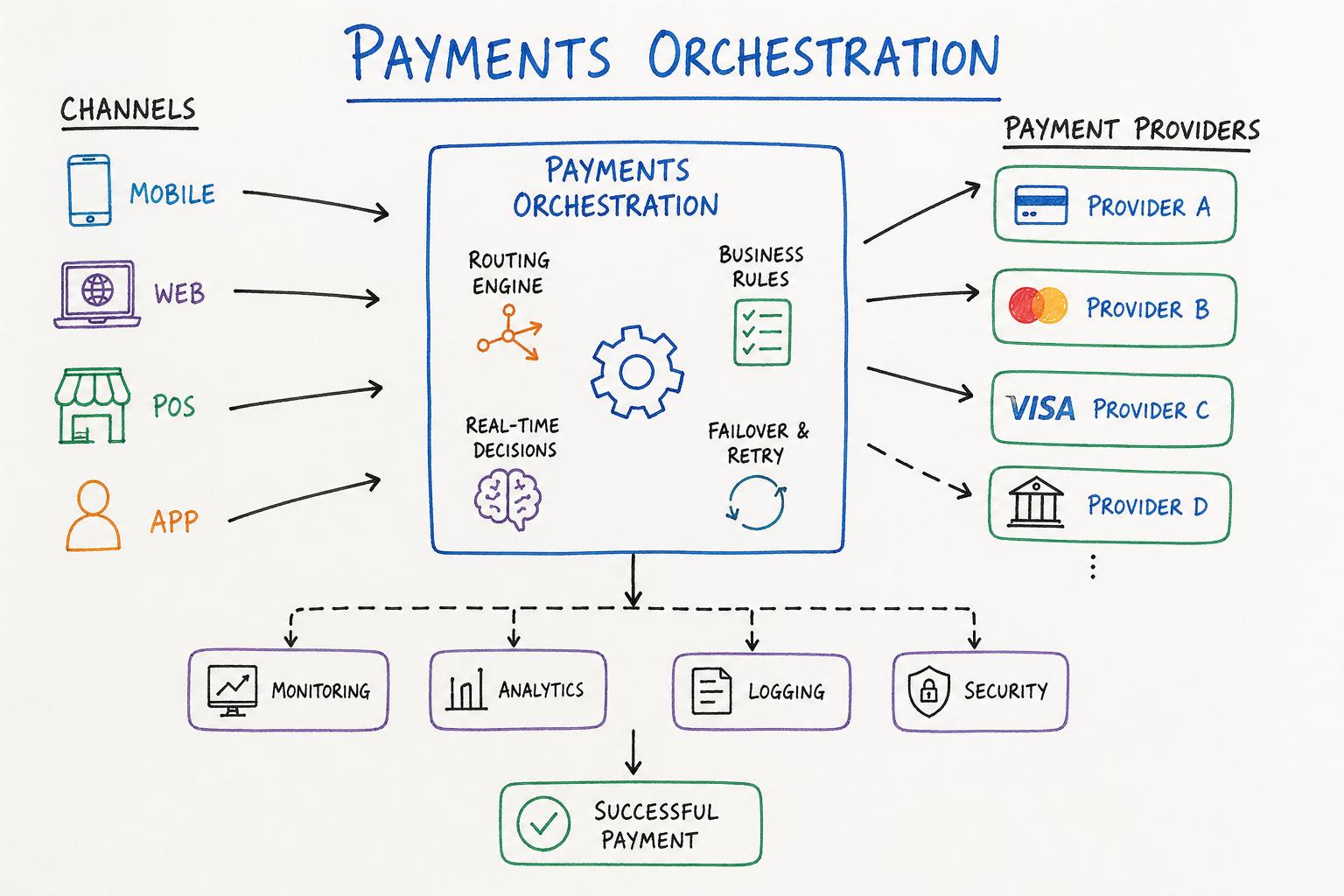

What Is Payment Orchestration?

Payment orchestration is the technology layer that centrally manages multiple payment gateways, banks and payment methods through a single platform. It goes beyond the PSP model — the business defines rules for which transaction goes to which channel.

Core orchestration capabilities:

- Smart Routing: Each transaction is sent to the channel with the highest success rate and lowest cost.

- Cascading: Failed transactions are automatically retried on an alternative bank.

- Multi-Bank Management: All bank integrations managed through a single API.

- Automated Reconciliation: All channels reconciled centrally.

- Tokenisation: PCI DSS compliant card storage valid across all channels.

Which Model Does Your Business Need?

- Small / new e-commerce: Start with a PSP for fast time-to-market.

- Growing platform: When multi-bank needs emerge, evaluate payment orchestration.

- Marketplace: Sub-merchant management requires orchestration with a marketplace module.

- Enterprise / Fintech: Full orchestration, secure card storage, e-money infrastructure.

Conclusion

Payment system infrastructure — gateway, PSP and orchestration — consists of interconnected layers. Choosing the right model for your scale and needs directly impacts payment success rates and long-term costs.

Explore Treps payment orchestration solutions at our solutions page.